Within the newest Solana information, SOFIUSD, a dollar-pegged stablecoin launched by SoFi, a publicly traded, bank-chartered fintech with 15.4 million members, on each the Ethereum and Solana networks in early 2026.

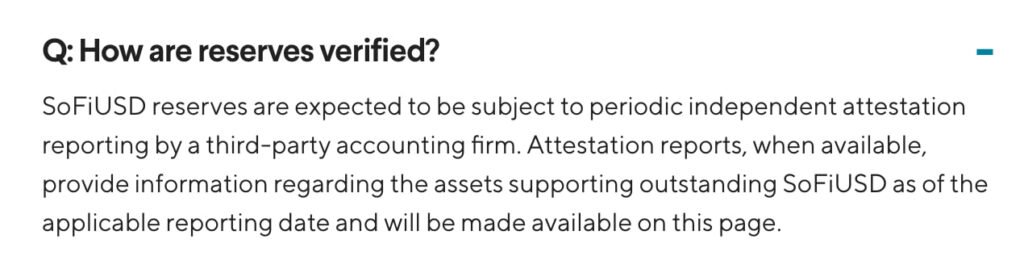

Each token is backed 1:1 by a reserve portfolio consisting of 85% short-term U.S. Treasury payments and 15% money held at FDIC-insured establishments, with these reserves verified month-to-month by Deloitte and held in segregated accounts on the Federal Reserve Financial institution of San Francisco.

Right here is the central stress this text unpacks: the phrase “regulated” will get hooked up to plenty of monetary merchandise, however for retail buyers contemplating SOFIUSD, what that label really means in apply, what it protects, what it doesn’t shield, and the way it compares to present choices like USDC or USDT, is value understanding clearly earlier than you progress a single greenback in.

Say “hello” to SoFiUSD (SoFiD)

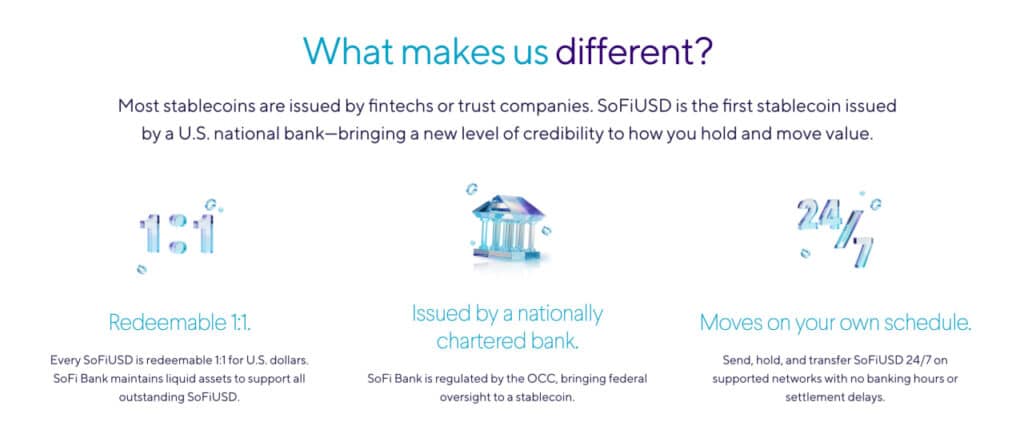

The primary stablecoin issued by a U.S. nationwide financial institution and redeemable 1:1 for money or money equivalents. Rolling out now, it’s constructed for a way cash strikes at this time: quick, versatile, 24/7. pic.twitter.com/I0eHIxDR50

— SoFi (@SoFi) Might 27, 2026

DISCOVER: The Subsequent 1000x Crypto Gem Earlier than It Lists on Binance

Solana Information: What’s SOFIUSD? The Plain-English Clarification

Consider SOFIUSD like a digital declare ticket for an actual greenback sitting in a government-supervised vault. If you maintain one SOFIUSD token, SoFi is required by regulation to carry one greenback’s value of U.S. Treasury-backed property in your behalf.

The token itself lives on a blockchain, both Ethereum or Solana, however the worth behind it by no means leaves regulated monetary infrastructure.

The 1:1 peg implies that one SOFIUSD ought to at all times be redeemable for one US greenback, and the Stablecoin Transparency and Accountability Act signed into regulation in late 2025 legally requires SoFi to honor that redemption inside two enterprise days.

That’s meaningfully totally different from an algorithmic stablecoin, which tries to keep up its peg via code and market incentives reasonably than precise greenback reserves, a mannequin that collapsed catastrophically with TerraUSD in 2022.

The U.S. Treasury-backed reserve construction additionally distinguishes SOFIUSD from earlier stablecoins that saved their backing opaque. Tether, the issuer behind USDT, spent years going through questions on whether or not its reserves had been actual and totally liquid. SoFi publishes its reserve composition day by day on its web site, which is an ordinary fully totally different from the one utilized by different banks.

On the technical facet, SOFIUSD is issued as an ERC-20 token on Ethereum for institutional-grade use, and as an SPL token on Solana for quick, low-cost retail transactions, and Solana’s Q1 2026 community information reveals why that chain issues for payment-speed stablecoin use circumstances.

DISCOVER: Finest Meme Coin ICOs to Spend money on 2026

What Does ‘Regulated’ Standing Truly Imply for Retail Traders?

The phrase “regulated” does actual work right here, however provided that you perceive what it covers. SoFi is supervised by the Workplace of the Comptroller of the Foreign money as a nationally chartered financial institution, the identical regulatory class as conventional banks – which implies it already meets capital necessities and client safety requirements that almost all crypto-native stablecoin issuers have spent years making an attempt to copy via state-by-state cash transmitter licenses.

In concrete phrases, the regulated stablecoin construction supplies three significant protections that an unregulated or offshore issuer can not supply:

Reserve transparency: Month-to-month SOC 2 Sort II attestations by Deloitte confirm that the reserves backing each SOFIUSD token really exist and are composed as acknowledged. You aren’t trusting a press launch; you’re trusting an audited report from a registered accounting agency.

Redemption assure: The Stablecoin Transparency and Accountability Act requires a full redemption inside two enterprise days. SoFi processes these via the identical ACH and wire methods it already makes use of for normal withdrawals, so the infrastructure exists and is examined.

Segregated reserves: The property backing SOFIUSD are held in segregated accounts, that means they’re legally separated from SoFi’s working capital. If SoFi confronted monetary problem, these reserves wouldn’t be obtainable to collectors; they exist solely to again the tokens.

What regulated standing does NOT assure is equally necessary to call. SOFIUSD just isn’t FDIC insured, SoFi’s personal disclosures say so explicitly. It doesn’t eradicate good contract danger, the place a bug within the token’s code may theoretically be exploited.

It doesn’t shield towards chain-level disruptions on Ethereum or Solana. And the 4.2% APY promotional yield provided throughout launch is funded by Treasury reserve earnings, which implies it could possibly change as rate of interest circumstances shift. Regulation raises the ground; it doesn’t take away each ceiling.

For added context on why regulated standing issues within the broader crypto panorama, the ARMA Invoice explainer covers how U.S. regulatory frameworks are reshaping the way in which digital property are categorised and supervised, related background for anybody making an attempt to know why a financial institution constitution modifications the danger profile of a stablecoin issuer.

Observe 99Bitcoins on X For the Newest Market Updates and Subscribe on YouTube For Every day Knowledgeable Market Evaluation.

The publish Solana Information: SoFi Simply Launched a Financial institution-Backed Stablecoin With Month-to-month Audits and a 4.2% Yield appeared first on 99Bitcoins.

{kind=link}