Technique has launched a brand new convertible bond providing price greater than $500M, and for the primary time since Michael Saylor pivoted the corporate towards Bitcoin in 2020, the SEC submitting lists “normal company functions” as the first use of proceeds, with no specific mandate to purchase extra Bitcoin.

That single change in language is sufficiently small to miss and vital sufficient to reshape how buyers take into consideration MSTR. Right here is the central rigidity this text unpacks: Is the Saylor playbook evolving into one thing extra sustainable, or has the corporate quietly hit a ceiling on its leverage technique?

This query about the way forward for the only largest holder of Bitcoin comes as BTC USD is buying and selling at $77,250, up round 1% on the day, because the market exhibits indicators of life following a interval of consolidation.

Technique Stories No #Bitcoin Buy This Week, Provides Bonds As a substitute. $BTC

A chart shared confirmed that as of Could 24, 2026, Technique’s Bitcoin reserves have been valued at roughly $64.45 billion. The corporate holds 843,738 BTC in whole, acquired at a mean price of $75,701, and… pic.twitter.com/QtH5je2oFK

— TheCryptoBasic (@thecryptobasic) Could 25, 2026

Technique Bond Information: What Does Skipping Bitcoin Really Sign?

MicroStrategy’s bond offers will be likened to a house owner remortgaging to purchase extra property, with the money particularly used for buying

Bitcoin. Since mid-2020, the corporate has raised over $7Bn by means of convertible bonds, which bondholders can convert into inventory if the value reaches a sure degree.

Every fundraising effort was designated for Bitcoin, making a cycle of borrowing, shopping for BTC, and watching each Bitcoin and MSTR inventory rise.

These zero-coupon convertible notes pay no common curiosity; as an alternative, buyers revenue by changing their bonds into MSTR inventory at a preset value.

As an example, a $3Bn tranche of notes due 2029 had a conversion value of $672.40 per share. At the moment, MicroStrategy’s whole debt exceeds $4Bn, with maturities spanning 2027 to 2030.

Nevertheless, the brand new providing deviates from the earlier sample. It mentions “normal company functions,” which might embody numerous makes use of however doesn’t embrace the acquisition of Bitcoin.

This transformation is important, because the funding technique for MSTR bondholders and fairness holders has relied on the expectation that new capital would proceed flowing into Bitcoin.

(SOURCE: CoinGecko)

Is This a Strategic Pivot or Simply Accountable Steadiness Sheet Administration?

As of at present (Could 25, 2026), Technique holds 843,738 Bitcoin, valued at greater than $65Bn, largely by means of a convertible debt technique that Saylor has adopted over the previous few years.

Just lately, the corporate agreed to repurchase about $1.5 billion of its 0% 2029 convertible notes for an estimated $1.38 billion, indicating a shift in the direction of legal responsibility administration as an alternative of additional accumulation.

This transfer, together with impartial language in a brand new submitting, suggests a stability between sustaining a wholesome stability sheet and Bitcoin purchases.

Analysts have blended opinions: some see it as a dangerous “convertible debt scheme,” whereas others view it as a strategic fusion of capital markets and a long-term Bitcoin funding. The important thing query now could be which section the corporate is getting into.

DISCOVER: 10+ Subsequent Crypto to 100X In 2025

Can MSTR Maintain Its Premium because the Bond Playbook Shifts?

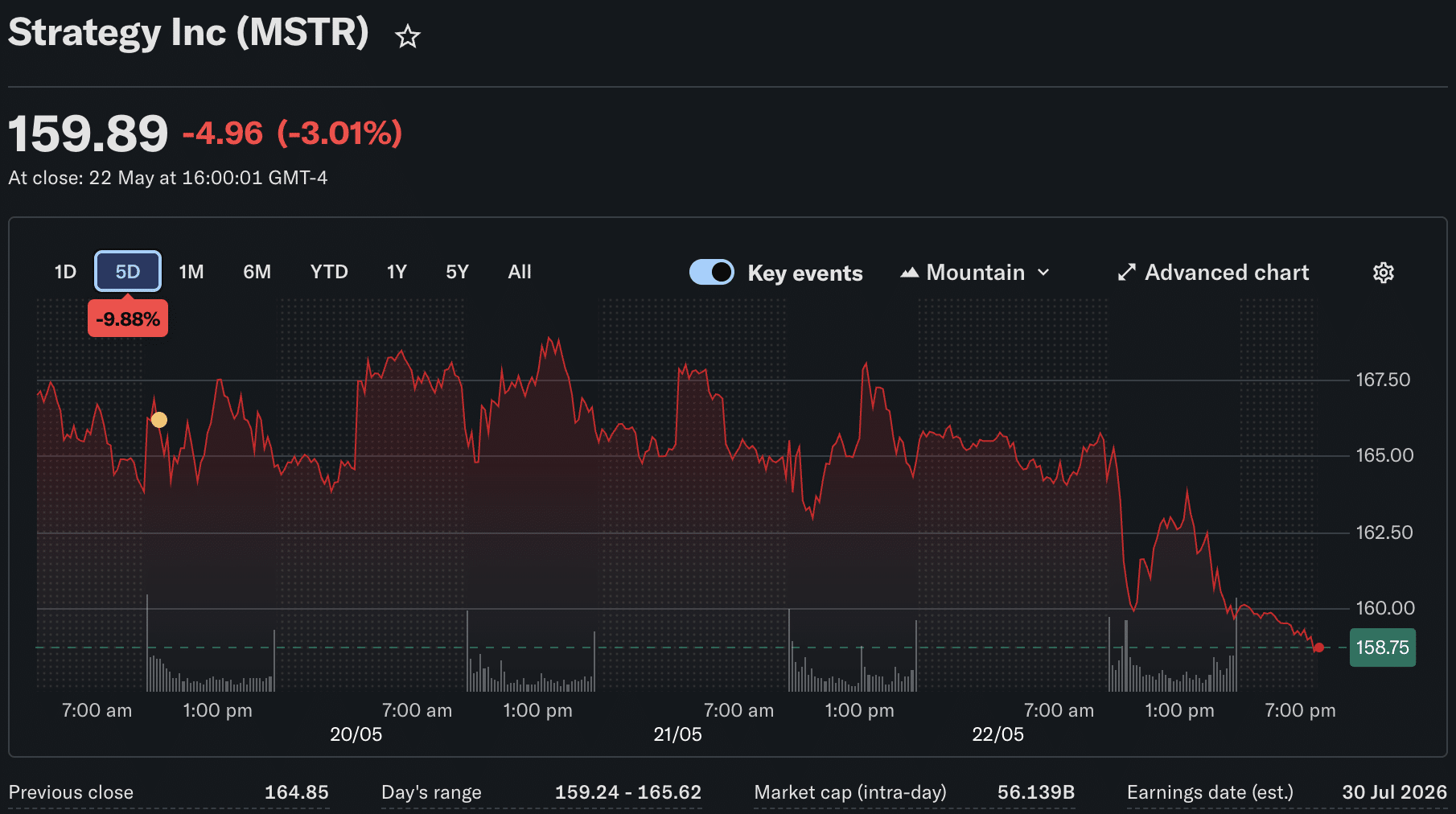

(SOURCE: Yahoo Finance)

On the time of writing, MSTR has traditionally traded at a big premium to the online asset worth of its Bitcoin holdings – generally as excessive as 2x or 3x the underlying BTC worth.

That premium exists exactly as a result of buyers have handled the inventory as a leveraged Bitcoin car with a perpetual accumulation engine beneath it. If new capital is not flowing into BTC, that engine argument weakens.

Three numbers are price watching carefully. First, MSTR’s premium-to-NAV: if it compresses meaningfully towards 1x, that alerts the market is repricing the corporate as a Bitcoin holding firm relatively than a Bitcoin accumulation machine.

Second, the conversion thresholds on current notes, the 2030 tranche, as an example, solely permit conversion if MSTR trades above roughly $433.43, with early name provisions above $996.89. These ranges create pure rigidity factors within the inventory.

Third, Bitcoin’s value trajectory issues; present BTC market volatility instantly impacts whether or not MSTR’s current holdings are appreciating or creating new balance-sheet stress.

EXPLORE: Greatest Crypto Presales Gaining Traction Proper Now

Observe 99Bitcoins on X, YouTube, and Telegram for extra crypto information and evaluation.

The submit Bitcoin Information: Has Saylor Simply Modified the MicroStrategy Playbook? appeared first on 99Bitcoins.

{kind=link}