Analyst Weekly, February 2, 2026

Earnings Preview: Week of February 2nd

Earnings this week will check whether or not AI momentum and resilient demand can maintain large-cap development on monitor. For many shares, steerage and ahead commentary matter greater than the quarter simply reported.

Palantir Applied sciences (PLTR)

Merchants anticipate a major inventory transfer round earnings, with choices pricing implying no less than ~9% potential day by day volatility following the report; the inventory has been softer just lately regardless of robust good points in 2025.

Income development acceleration (anticipated >60% YoY) and AI platform adoption, particularly energy in industrial and authorities contracts, might be key drivers buyers watch within the outcomes.

Steerage and commentary on industrial AI demand and deal momentum (plus readability on longer-duration authorities contracts) might be focal matters for analysts and the market.

Amazon (AMZN)

Surging AWS cloud demand (pushed by AI workloads) plus aggressive price cuts have set the stage for a possible earnings beat and inventory soar.

AWS income development is the highest metric: consensus sees cloud accelerating (~24% FY2026 development vs ~21% prior) due to AI-driven utilization.

On the decision, buyers will search perception into 2026 margin steerage and cloud momentum: particularly how AI infrastructure investments and up to date layoffs will bolster profitability.

Alphabet (GOOGL)

Promoting and cloud are the dual engines to observe for Google’s dad or mum.

A strong vacation quarter for advert income, together with strong search queries and YouTube viewership, and enchancment in Google Cloud’s gross sales may elevate the inventory

The decision will possible spotlight YouTube and Search, with buyers listening for updates on advert demand, price self-discipline, and the way AI improvements (in search and promoting instruments) are shaping Google’s technique going ahead.

Superior Micro Gadgets (AMD)

As a bellwether for the chip trade, AMD’s data-center and PC processor gross sales will closely affect its inventory.

A robust demand for EPYC server chips or console processors may drive an upside shock, whereas any weak spot in consumer PC or GPU gross sales would possibly weigh on sentiment.

Traders will give attention to revenue margins and steerage, particularly amid intense competitors with Intel and Nvidia: for instance, whether or not AMD’s newest AI and graphics merchandise are gaining traction.

PayPal (PYPL)

Branded Checkout development: Anticipated at ~2–3% in 4Q; any miss would possible weigh on the inventory.

Traders need early indicators that AI, BNPL and new checkout options can drive utilization with out hurting near-term development.

2026 outlook: The inventory will react to branded development steerage and affirmation that enormous buybacks proceed to assist EPS through the funding yr.

Walt Disney (DIS)

The inventory’s response will depend upon core section efficiency and ahead technique.

Traders might be anticipating indicators of streaming turnaround, corresponding to Disney+ subscriber development or narrower streaming losses

Key factors on the decision embrace Disney’s streaming profitability timeline, theme park demand and margins, and updates on strategic initiatives (like plans for ESPN or Hulu) that might form future development

Merck & Co. (MRK)

The destiny of Merck’s blockbuster medication will set the tone for its earnings response.

Its most cancers immunotherapy Keytruda (the corporate’s prime vendor) and HPV vaccine Gardasil stay essential.

Traders are laser-focused on how Merck is making ready for looming patent cliffs (Keytruda loses exclusivity later this decade).

Pfizer Inc. (PFE)

The inventory’s response might be pushed by how properly Pfizer’s core portfolio and new launches (e.g. RSV vaccine Abrysvo, migraine remedy Nurtec, oncology medication from the Seagen acquisition) are filling within the hole.

The corporate faces a major patent cliff within the coming years (main merchandise like Eliquis, Ibrance, and Xtandi face exclusivity losses, with an estimated ~$1.5B income hit already anticipated in 2026).

Eli Lilly (LLY)

Lilly’s earnings might be dominated by the spectacular development of its GLP-1 medication for diabetes and weight problems.

Its twin blockbusters, Mounjaro (tirzepatide for kind 2 diabetes, additionally bought as Zepbound for weight reduction), have grow to be the top-line drivers, contributing over half of Lilly’s income thus far in 2025.

An enormous earnings beat may come if gross sales of Mounjaro/Zepbound exceed expectations but once more.

Traders will wish to hear if demand continues to be outpacing provide, how the launch of Novo Nordisk’s new oral rival (oral Wegovy) would possibly have an effect on Lilly, and when Lilly’s personal oral GLP-1 (orforglipron) may attain the market

Uber (UBER)

The inventory will react as to if Mobility journey development stays close to high-teens (~19% YoY)

Traders will see if profitability holds as Uber reinvests insurance coverage financial savings and affordability initiatives.

AV narrative vs fundamentals: Commentary on autonomous car threat (Waymo, Tesla) issues, however sustained quantity development is the important thing offset buyers need confirmed on the decision.

Shell plc (SHEL)

Oil and buying and selling weak spot: Decrease oil costs and softer buying and selling outcomes level to weaker This fall earnings versus Q3.

Gasoline offset: Larger winter fuel costs could assist LNG and fuel earnings.

Capital returns: The inventory will hinge on buyback/dividend steerage and any indicators on capital allocation underneath the brand new CEO.

What A Warsh Fed Means For Asset Courses & Sectors

Markets typically speak about new Fed chairs when it comes to “hawk vs dove,” however that framing misses the actual shift. A Warsh Fed will not be the market shock some worry, and it’s not a return to ultra-easy coverage both. As an alternative, it indicators a change in how assist is delivered.

Somewhat than relying closely on balance-sheet growth and detailed ahead steerage, a Warsh Fed would possible place extra emphasis on market pricing, personal capital, and fundamentals. Rates of interest should transfer decrease, however the Fed is much less more likely to easy each market transfer or pre-signal coverage far upfront.

We now anticipate to see:

A smaller, shorter-duration steadiness sheet. Importantly, this shift is more likely to be gradual, aimed toward lowering distortions over time quite than tightening monetary situations abruptly

A shift of reserve intermediation again to non-public banks

Coordination of balance-sheet discount with Treasury (and probably housing businesses)

Shift the Fed’s holdings towards shorter-duration property, nearer to the pre-GFC mannequin

Funding Takeaway: We anticipate a gradual transition to a market-driven system the place costs are set extra by fundamentals and personal capital, and fewer by central-bank assist, signalling, or balance-sheet intervention.

In sensible phrases, underneath a Warsh-Fed this possible means:

Much less reliance on Fed balance-sheet growth to stabilise markets.

Much less ahead steerage telling buyers the place charges might be months forward.

Extra weight positioned on precise knowledge, earnings, money flows, and steadiness sheets.

Property most delicate to central financial institution QE, like Treasuries, MBS, and actual property, will react extra to this than to nominal charge adjustments.

This might be a basic shift. Asset class implications are;

Charges transfer decrease, however this isn’t a period bonanza

Warsh will possible vote for 1 to 2 charge cuts shortly, probably a 3rd towards impartial.

Nevertheless:

He’s targeted on inflation expectations, not simply the coverage charge

Stability-sheet self-discipline limits how far long-end yields can fall

Stability-sheet coverage could matter greater than charge cuts

Fed steadiness sheet shrinks provided that personal steadiness sheets can increase

Deregulation permits banks to soak up liquidity and Treasury provide.If deregulation falls quick, balance-sheet discount may translate into tighter monetary situations and episodic bond market volatility.

Market implication:

Actual yields and time period premia, not simply charge cuts, will stay key drivers of long-term bond efficiency.

Treasuries: delicate to deregulation follow-through

Entrance-end and stomach of the curve profit

Lengthy-duration Treasuries could face capped upside

This can be a curve and carry commerce, not an outright period wager

Funding-grade credit score stays higher supported than lower-quality excessive yield, the place the Fed is much less more likely to act as a backstop.

Equities: dispersion replaces beta

Warsh Fed will not be a hawkish shock, however a structural shift away from blanket liquidity.

That will have implications for fairness management.

Beneficiaries:

Financials & Banks : deregulation + balance-sheet normalization

Worth / cyclicals: profit from modest easing with out extra liquidity

Insurers & asset managers: greater long-end yields, much less Fed distortion

Market implication:

Inventory choice issues greater than index publicity

Extra speculative, extremely leveraged, or long-duration development shares could face a more durable surroundings with out broad liquidity assist.

Greenback and FX: stability over weak spot

Warsh cuts charges, however preserves:

Inflation credibility

Stability-sheet self-discipline

That’s not a basic dollar-bearish combine.

Market implication:

Greenback possible range-bound to agency

FX dispersion will increase vs low-credibility currencies

Volatility could rise as steerage fades

Warsh is much less inclined towards heavy ahead steerage.

Markets lose:

Predictable signaling

Coverage “coaching wheels”

Market implication:

Larger macro and coverage volatility

Better worth in:

Diversification

Volatility-aware methods

Systematic approaches

Funding Takeaway: Taken collectively, a Warsh Fed represents a shift away from blanket liquidity assist and towards market-driven pricing throughout asset courses. Charges could transfer decrease, however balance-sheet self-discipline limits upside for long-duration bonds. Credit score turns into extra selective, equities see better dispersion, and sectors tied to non-public capital and balance-sheet energy, significantly financials, acquire relative significance. Lowered ahead steerage raises volatility, but additionally will increase the worth of diversification and lively positioning. For markets, this is probably not a tightening shock, however a rebalancing of how threat is priced, the place fundamentals, money flows, and steadiness sheets matter greater than central-bank signaling.

Bitcoin and ethereum are present process a liquidity-driven adjustment, not a thesis breakdown.

The current transfer displays a convergence of institutional outflows, pressured deleveraging, and contracting base liquidity, amplified by a fragile macro backdrop.

For the primary time since spot ETFs launched, three consecutive months of internet promoting have eliminated assist close to institutional price ranges (~$98k), triggering $1.8bn in liquidations, overwhelmingly on the lengthy facet. On the similar time, long-term holders are distributing, including provide right into a market with decreased absorption capability as stablecoin liquidity tightens.

With Bitcoin nonetheless extremely correlated to large-cap tech and macro uncertainty elevated, key ranges now outline the regime:

$85k because the fast threat threshold, $75k as near-term assist, and $50k–$60k because the potential decision zone if the adjustment continues.

Palantir After the Promote-Off: Will the Key Help Maintain?

Palantir shares got here underneath vital stress final week, falling by 13.4%. A equally sharp decline was final seen in March. Consequently, the gap to the all-time excessive has widened to round 32%. The inventory dropped to $146.59, a degree first reached in June and one which already acted as an necessary assist space in August.

Slightly below this degree lies one other technically related zone. Between $138.66 and $144.85 is a so-called truthful worth hole, inserting the inventory in a decisive technical space at current.

The calendar provides additional significance. Palantir will report its quarterly outcomes after market shut on Monday, that are more likely to act as a catalyst for the following main transfer.

In a constructive state of affairs, a part of final week’s losses might be recovered. A transfer towards the 20-week shifting common, at present at $169.48, could be attainable. A return above this degree would ease the technical image.

In a detrimental state of affairs, nevertheless, a break beneath the present assist may set off additional promoting stress. In that case, there could be little in the way in which of near-term assist, with the following related assist zone—one other truthful worth hole—solely between $98.81 and $108.73.

Palantir, weekly chart. Supply: eToro

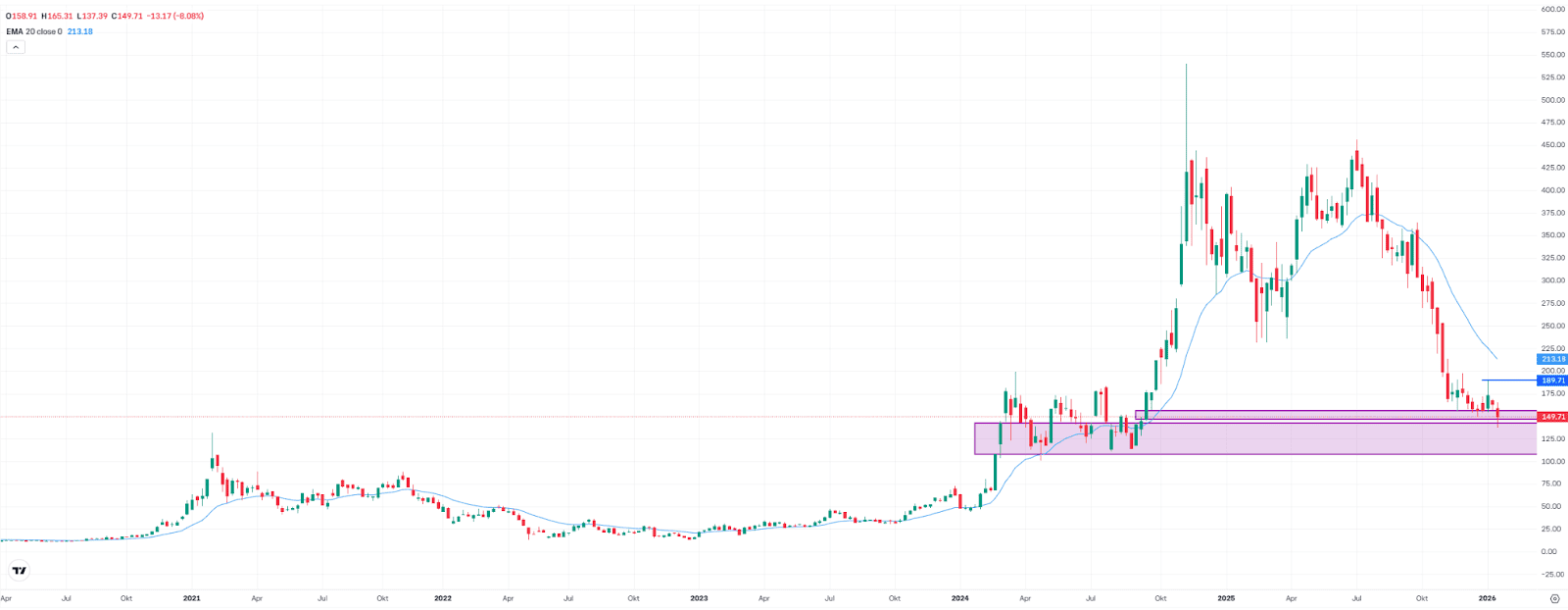

Lowest Stage Since 2024: Technique Struggles for Technical Stabilization

Technique shares additionally got here underneath notable stress final week, falling by 8.1% to $149.71. This marked the bottom degree since September 2024. The hole to the file excessive has now widened to greater than 70%.

No less than within the quick time period, there was a primary constructive sign. The rebound on Friday ensured that two necessary assist zones have been revered. Each the truthful worth hole between $148.67 and $156.84 and the decrease zone between $107.83 and $143.59 held. This provides some encouragement, regardless that stabilization doesn’t but imply the all-clear. The market may nonetheless transfer decrease, however an preliminary necessary technical step has been taken.

Consideration now turns to Thursday night. Technique will launch its This fall outcomes and outlook after the shut, that are more likely to decide whether or not stabilization continues or promoting stress returns.

To sustainably enhance the chart image, a transfer above the short-term excessive at $189.84 could be required. A return above the 20-week shifting common, at present round $213, may function further affirmation. Till then, the scenario stays fragile. The danger stays excessive that the inventory may slip deeper into the second assist zone.

Technique, weekly chart. Supply: eToro

This communication is for info and training functions solely and shouldn’t be taken as funding recommendation, a private advice, or a proposal of, or solicitation to purchase or promote, any monetary devices. This materials has been ready with out bearing in mind any explicit recipient’s funding aims or monetary scenario and has not been ready in accordance with the authorized and regulatory necessities to advertise unbiased analysis. Any references to previous or future efficiency of a monetary instrument, index or a packaged funding product should not, and shouldn’t be taken as, a dependable indicator of future outcomes. eToro makes no illustration and assumes no legal responsibility as to the accuracy or completeness of the content material of this publication.

{kind=link}